-

News

-

Blog

-

Archive

When year-end rolls around, the last thing you want as a business owner is finding yourself fishing for receipts, counting stock, and scrambling to meet HMRC deadlines.

After all, nothing matters more than getting your accounts straight by this point, not just to avoid hefty HMRC penalties but also to see clearly how your business really performed this year.

To make life easier, I've put together a straightforward retail accounting checklist. It's designed to keep tax prep simple and stress-free.

And if it all starts to feel like too much, no need to worry. You can always lean on a small business accountant who'll take the pressure off so you can stay focused on running and growing your business while the books are tidied up in the background.

Want to steer clear of HMRC penalties and finally get your books in order before deadlines? Have a chat with a professional small business accountant Bolton.

Here's the checklist:

#1 Get Ready for Tax Filing

Nobody looks forward to tax season, but it doesn't have to be a nightmare. With a bit of prep, you can avoid last-minute stress, keep HMRC happy, and maybe even save yourself some money. Here's what to tick off:

- Round up your records: Pull together invoices, receipts, bank and credit card statements, and payroll records. Keeping them in order (by date or category) makes life a whole lot easier.

- Check your sales: Make sure all sales are logged, whether they came from your shop, online, or other channels. Double-check VAT calculations so nothing slips through.

- Sort your expenses: List out everything you've spent on the business this year. Rent, utilities, stock, marketing, many of these are tax-deductible, so don't miss out.

- Look at big purchases: If you've bought equipment, vehicles, or shop fittings, you may be able to claim capital allowances (basically tax relief on assets).

- Tidy up VAT returns: If you're VAT-registered, reconcile your VAT account and get that final return for the year lined up.

- Get expert eyes on it: A professional accountant can spot tax-saving opportunities you might miss and make sure you're fully compliant.

#2 Check Your Bank and Accounts

Now, you need to make sure what's in your records matches what's actually happening in your bank. Why? Because it helps catch errors before they snowball.

- Match up your bank statements: Compare your bank records with your accounting system. Identify any differences (like missing payments or outstanding cheques) and fix them as you go.

- Review credit card statements: Make sure every card transaction is logged and filed under the right category.

- Chase unpaid invoices: Check your accounts receivable (the money owed to you) matches your records. If anything's overdue, follow up.

- Check your bills: Do the same with accounts payable (what you owe suppliers). Confirm every bill is logged and nothing's missed.

- Tidy up loan accounts: Make sure loan repayments (interest + principal) match what your lender shows.

#3 Count and Value Your Stock

Understandably, year-end stocktaking might feel like a chore, but it's one of the most important steps for retailers. It tells you what you've really got on hand, helps prevent loss, and ensures your accounts are accurate.

- Pick the right time: Do your stocktake when things are quiet or the shop's closed, so you're not distracted.

- Get organised first: Label items clearly and tidy up the storage area to make counting easier.

- Do a physical count: Go through every item, whether it's on the shelves, in storage, or in transit.

- Record it properly: Note down item names, quantities, and locations. A spreadsheet or stock software helps speed things up.

- Compare with your system: Match your physical count against your accounting records. Fix any gaps or errors you spot.

- Adjust for reality: Write off damaged or unsellable stock so your numbers reflect the true picture.

- Work out COGS: Once your stock is accurate, calculate your cost of goods sold (basically: opening stock + purchases – closing stock).

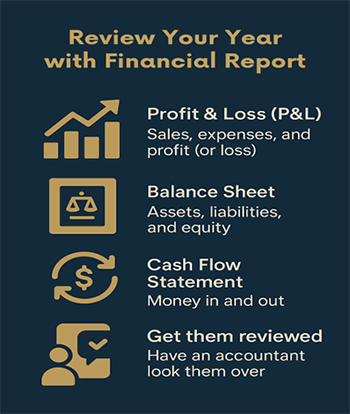

#4. Review Your Year with Financial Reports

Your reports are more than just numbers on a page, they tell the story of how your business performed this year. Having clear, accurate reports helps you make better decisions and keeps you compliant.

- Profit & Loss (P&L): Shows your sales, expenses, and profit (or loss) for the year.

- Balance Sheet: A snapshot of your business's health: what you own (assets), what you owe (liabilities), and what's left (equity).

- Cash Flow Statement: Tracks how money moved in and out. Vital for spotting cash gaps even if profits look healthy.

- Check your margins: Look at simple ratios like gross profit margin and net profit margin to see how efficiently you're running.

- Add notes if needed: Sometimes reports need explanations, like unusual expenses or changes in accounting methods.

- Stay compliant: Make sure your reports meet UK accounting standards.

- Get them reviewed: Having an accountant look over your reports can highlight blind spots and save you from costly mistakes.

Wrap Up Your Year with Confidence

With this checklist, you'll stay organised, avoid HMRC penalties, and get a clear picture of how your business is really doing. And with the right support, you can close your year with confidence and peace of mind. Want to take it off your plate? Reach out to a small business accountant in Bolton who is only a call away.